Open banking architecture is the key to enabling the more accessible, convenient, and customer-focused digital banking services that we all enjoy today.

By facilitating seamless data exchange between banks, this technology has given consumers more control over their finances than ever before. The vast amount of finance management and payment processing apps available in 2023 is evidence of the influence and success of open banking systems.

Of course, the unrestricted flow of financial information also creates certain risks. Without effective authentication mechanisms, cybercriminals can easily target critical data. It’s no surprise, then, that a far-reaching regulatory environment is essential for the success of this financial architecture.

On this page, we’ll take an in-depth look at open banking architecture, exploring the benefits for consumers and businesses as well as how its risks can be mitigated.

What is open banking architecture?

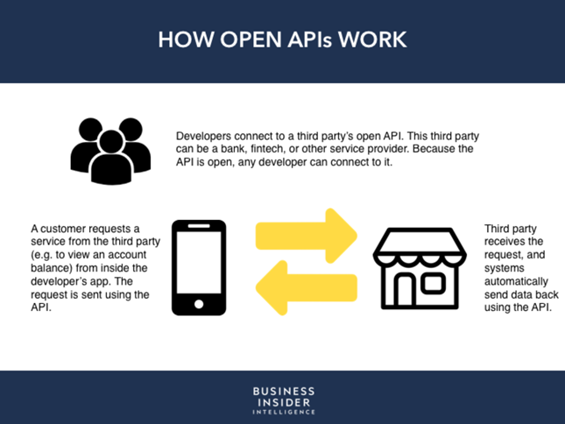

The purpose of open banking is to break down the barriers that exist in the world of finance. It does this by connecting financial data from traditionally separate sources, such as an individual’s multiple bank accounts, payment cards, and mobile wallets. Without getting too technical, this data can be ‘fetched’ through the use of open banking API services.

The result of using open banking systems is that users can see all their financial data in one place (think of finance management apps like Mint) and even initiate payments from their bank using third-party apps (with the most famous example being PayPal).

Businesses can also benefit from more accessible financial information, for example, it can allow money lending companies to quickly and easily assess the creditworthiness of applicants.

Open banking started when the concept of financial data aggregation first emerged in the mid-1990s. This was the idea that users should be able to use a single sign-on (SSO) to access and manage all their funds.

Early aggregator software, like Vertical One and Yodel, used a method called screen scraping to fetch data that wasn’t provided through API links due to the systems used by banks being outdated.

However, early financial data aggregators were inaccessible to ordinary folk and also suffered from a lack of strong security. In the 2000s, the rollout of mobile banking apps standardized financial data access and the development of APIs for legacy systems, making it much easier for users to check account balances or transfer funds on the go.

Following the 2008 financial crisis, challenger banks began to break into the mainstream and took open banking to the next level. Self-styled “neobanks”, such as Starling and Chime, provided users with real-time phone notifications when a transaction was made, including details like who the payee was and options to dispute an unrecognized payment. This idea caught on fast.

Today, you’ll likely hear these sorts of organizations (and their software) referred to as “fintech”. However, open architecture doesn’t exclude traditional banking institutions. In fact, the EU’s 2018 Payment Services Directive mandated that all European banks must provide open access to their customers’ data through APIs. This was obviously a watershed moment for the technology and its application.

Open banking now appears to have a bright future, with banks, businesses, and individuals all benefiting from its applications. However, it’s vital that the risks are understood to ensure that financial institutions don’t become victims of their own innovation.

How can open banking infrastructure benefit users?

We’ve established that open banking infrastructure gives consumers more control over their finances, but how can banks and businesses benefit from this technology?

Banks

It might seem contradictory for a disruptive new technology like open banking to provide benefits for legacy banks, however, it actually creates a huge opportunity for banks to stand out from their competitors.

For example, legacy banks that innovate and adopt open banking features are likely to improve customer engagement and loyalty. There’s also the opportunity to create new revenue streams through partnerships with third-party providers.

Businesses

For businesses, the free flow of capital is almost always a good thing. It means they can offer more payment options to customers, reach new audiences, and gain easier access to finance for business growth.

As payment transactions can be sent directly from bank to bank, as opposed to through a debit or credit card network, they also tend to be quicker and cheaper.

Open banking has had a particularly positive impact on industries like insurance and money lending. Easy access to the financial data of customers means that applications can be processed faster and allows for the swift and secure delivery of personalized quotes.

Individuals

Above all, open banking benefits the end user. By removing the barriers that exist within traditional finance, consumers can move their money to, from, and between accounts with previously unheard-of ease.

Solutions like mobile finance apps and one-click sign-ins make money management more understandable and achievable for everyone. It's now easier to get insurance, take out loans, and pay for services—transactions that may have taken days to process with legacy architecture.

Open banking also means developers can build highly customizable apps, ensuring consumers are spoiled for choice with the variety of finance management options available.

Addressing the risks of open banking technology

Despite the considerable benefits of open banking technology, it’s important to also consider its risks.

Security

When it comes to digital innovation, data handlers must understand that with great power comes great responsibility.

This is especially true when institutions are handling peoples’ hard-earned money. Therein lies the biggest challenge with open banking—how can a system that enables the free flow of financial information also protect it from falling into the wrong hands?

To answer this question, cybersecurity experts focus on identifying vulnerable spots that hackers might try to manipulate. The first step is usually to create a secure API design that can detect malicious activity, analyze data request patterns, and automatically trigger alerts when conditions are breached.

Financial institutions need to stay one step ahead of the game at all times, which means constant reviews as well as penetration testing of the entire application lifecycle. The alternative is far more costly, as a data breach could result in a catastrophic lawsuit, regulatory fines, and a loss of customer trust.

Consent

A core principle in the world of finance (and data handling in general) is consent.

Open banking empowers users to take control of their data and use it for whatever means they see fit; it does not mean that third parties can snoop on anyone else’s personal information.

To achieve this, open banking API architecture has granular access controls that only allow entry when expressly confirmed by either the customer or the bank. The added security step of two-factor authentication (2FA) further prevents unauthorized requests in the case of situations like identity theft or stolen passwords.

Regulation

Regulatory oversight is how open banking systems are held to the expected standards. It’s these frameworks that guarantee accountability and responsibility in finance.

Banking is not typically a self-regulated industry. Rather, central governments recognize the importance of financial data security, with bodies like the European Banking Authority (EBA) and Consumer Financial Protection Bureau (CFPB) having extensive powers in their respective jurisdictions.

Standardization

Open banking is built on the premise that applications should be able to fetch data from multiple sources. To make this process easier, it makes sense for institutions to use compatible APIs, or else new code would need to be written for each data source.

It’s no surprise, then, that the need for API standardization plays a major role in initiatives like PSD2 in the EU and Financial Data Exchange (FDX) in the USA.

Integration

Another challenge with the transition to open banking is updating legacy architecture to meet modern standards.

Instead of rebuilding from the ground up, software engineers will often focus on systems integration as a bridge between old and new.

Implementing enterprise microservices architecture can be a particularly effective way to modularize legacy banking systems, enabling APIs to communicate smoothly with modern applications. The hardest part of the puzzle is arguably transforming financial data into a format that can be read by open banking APIs.

Open your banking architecture with OpenLegacy

To wrap up, open banking is currently on an upward trajectory, with new innovations and technologies making finance more accessible to everyone. Traditional banks don’t want to be left behind but can struggle to work out exactly how to move away from the legacy architectures that their systems are entirely built upon.

The answer isn’t to rebuild from scratch but rather to integrate your legacy systems using open APIs. This is our goal at OpenLegacy. We know that while maintaining your services’ data and core functionality is essential, you also need to develop agile new features that put your customers first.

Explore our successful case studies here, and see what OpenLegacy could do for your business.

Open banking architecture FAQs

What is open banking architecture innovation?

Open banking is a new model for financial architecture—one that focuses on cooperation between banks, networks, and application providers.

In order to stand out, financial institutions must constantly innovate and look for ways to improve their products. This has spurred the development of new features for consumers, such as real-time mobile banking, rapid credit score tests, and biometric sign-in authentication.

Is open banking secure?

Yes. Although the de-restricted exchange of financial data certainly poses risks, the strict regulatory environment it exists in ensures that open banking API architecture is secure. Data can only be transferred with direct authentication from the user or the user’s bank.

What is an example of an open banking system?

Nowadays, it’s possible to see elements of open banking in most areas of finance. That said, there are some standout examples of applications in this space.

For instance, services like Tully act as fully digital debt advice platforms that help people budget their finances. Revolut, on the other hand, lets you see external account balances and payments from one centralized platform. Or, to reduce transaction fees, Trustly provides an alternative payment method that speeds up the process of paying directly from your bank account.

We’d love to give you a demo.

Please leave us your details and we'll be in touch shortly